Australian Withholding Tax

for Visiting Performers and Sportspeople

Issues to be considered

1. Each overseas non-resident performer and sportsperson is subject to Australian income tax, either as an individual or as their corporate entity (the NR), with respect to income derived from services provided in Australia.

2. Tax is required to be withheld by the payer (the promoter/producer) and remitted to the Australian Taxation Office (ATO), (there are a number of administrative tasks which must be completed prior to earning the income and minimising the amount of tax that must otherwise be withheld and also to ensure compliance with the Australian tax rules see Procedural Matters below).

Summary of overall tax position

3. Non-resident corporations– these are generally subject to Australian tax on the net Australian-sourced profit at a flat rate of 30%. However a lower rate of 25% may apply if the corporation’s global gross income for the year ending June 2023 is A$50 million or less.

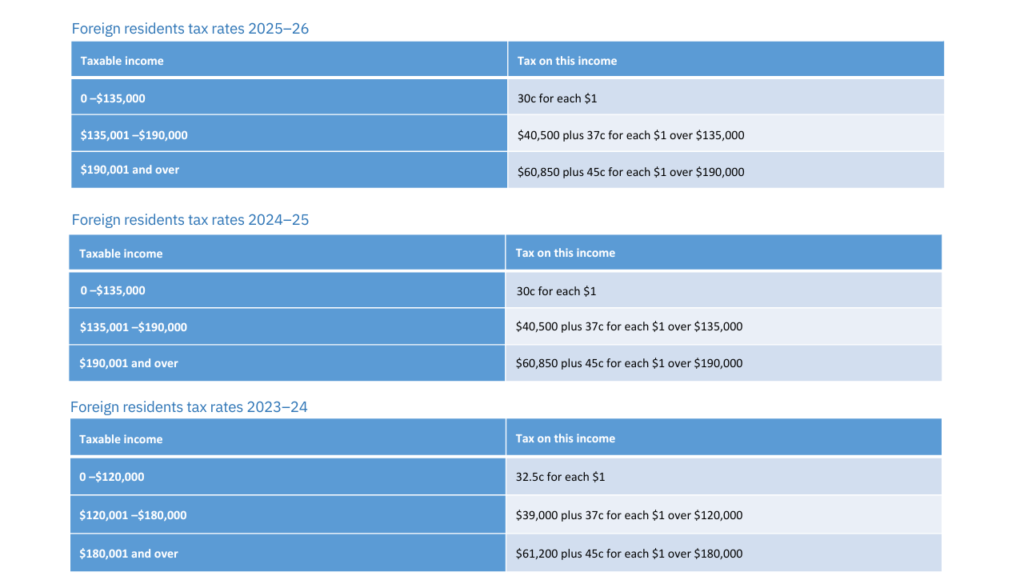

4. Non- resident Individuals– they are generally subject to Australian income tax on net Australian sourced income at non-resident individual tax rates ranging from –

5. Section 12-315 of Schedule 1 of the Taxation Administration Act 1953 (TAA) generally requires that the promoter must withhold tax on ANY component of the gross fee actually paid to the NR or its agent. Such tax must be remitted to the Australian Tax Office (ATO) by the 21st day of the month following that month in which a payment is made to the NR.

Notwithstanding, pursuant to Section 12-317 of Schedule 1 of the TAA fees and/or other income payable pursuant to a performance contract with NR (individual or other entity) may be paid to an intermediary, ABN-registered Australian agent who is appointed by the NR. In doing so, the agent accepts the withholding tax obligations associated with all payments it receives on behalf of the NR.

In these circumstance the agent must render the promoter/producer a valid Tax Invoice (inclusive of GST) for the relevant contract fee who will then be deemed to have complied with its payment obligations vis-a-vis the NR and will, simultaneously, be relieved of all related withholding tax obligation which now shift to the agent.

It is essential to note that pursuant to the withholding tax regulations the ATO considers that most payments to which the NR or its corporation fall within the definition of ‘gross fee’, i.e. contributions towards all costs including airfares, accommodation, production, per diems, etc.

Income from merchandising may be subject to withholding tax if it is earned by way of licensing agreement with the promoter/producer or local merchandiser. However, where such income is earned by way of a share of profit no withholding tax will apply.

Income from VIP packages/uplifts are also subject to withholding.

6. For individual tax residents of the United States, exemption under the USA/Australia Double Tax Agreement (DTA) may be applicable if the total fees earned (inclusive of per diems) are the equivalent of US$10,000 or less for each tax year ending 30 June. Other AUSTRALIAN DTAs do not have the same de minimis rule.

7. Goods & Services Tax (GST) (10%) – under GST amendments effective, 1 October, 2016, contracts between NRs and Australian Businesses do not have GST implications unless the NR is represented by an Australian GST agent (see below). The Australian agent brings a NR, or its entity, within the GST net and must invoice the promoter/producer appropriately. Recoupment of GST incurred by a NR on local/Australian expenses remains possible provided that the NR is appropriately registered or has appointed a local GST agent in a manner which gives it a fixed place of business in Australia. The appointment of a local agent is the preferred method of registration.

Procedural Matters

8. The NR may apply to the ATO to request a reduced rate of tax withholding (via a Foreign Resident Withholding Variation application– FRWV) to take into account the deductible expenses which are eligible to be claimed (e.g. agents’ fees, management fees, accommodation, travel etc. (where NR is responsible for these costs). If an FRWV is granted, tax (at the relevant corporate or personal tax rate) may be withheld based on the estimated net profit. This is usually achieved by engaging an Australian Tax Agent who is fully conversant with these processes.

9. Proof of Identity of Non-Resident Corporation/LLC/LLP – the relevant Certificate of Incorporation/Origin of a non-resident entity must be certified under the Apostille process before the ATO will proceed with the necessary ABN or TFN registration processes (see below). The Apostille-authenticated certificate should be received in Australia prior to the commencement of an engagement which involves a foreign entity, in digital format only.

10. Application for an Australian Business Number (ABN)– an ABN registration is required by all residents and non-residents (individuals and other entities) who wish to conduct business in Australia. An ABN is required to avoid tax being withheld AND/OR PAID at the maximum rate of 47% from any payment made to a NR. A tax File Number (see Point 11 below)) must first be allocated to a NR, individual or director/member of non-resident corporation/LCC, to facilitate the application for an ABN. The ATO will not impose the maximum rate of 47% on payments made prior to an ABN application being submitted in instances where the NR has formally engaged/appointed a local agent and instructed the agent to apply for an ABN on its behalf.

It is, therefore, essential that a NR who is entering to provide services in Australia for the first time should, as early as possible, formally engage a local tax agent and provide him with a copy of the passport of the director/member of the corporation/LLC who will be travelling to Australia together with a copy of the Certificate of Incorporation/Origin of the relevant corporation or LLC.

11. Application for an Australian Tax File Number (TFN)– in the case of a NR individual or director/member of a non-resident corporation/LLC/LLP, this is easily facilitated once he/she has passed through the first Australian immigration checkpoint. A copy of his/her passport will be required. In the case of a corporation an Apostille -certified copy of the company’s Certificate of Incorporation is also required by the ATO.

12. Unless exempt from Australian tax under a Double Tax Agreement (see Point 6 above), the NR must file a mandatory Australian income tax return to report the actual income/deductible expenses in circumstances where an FRWV has been granted (see Point 8 above). Any under/overpayment of tax will be settled at that time.

13. Upon completion of a tour, the promoter/producer will provide the NR with a Payment Summary, which discloses the total income earned in Australia (in Australian dollars) and the amount of tax withheld and to be remitted to the ATO. This document is submitted to the ATO with the final income tax return (see Point 12 above) to allow the tax withheld and paid by the promoter to be appropriately allocated/credited to the NR. NOTE: An income tax return cannot be filed if a TFN has not been issued to the NR.

14. Once the income tax return is lodged and assessed, a Notice of Assessment (Tax Certificate) will be issued by the ATO, which will provide the relevant proof of the foreign tax payment to be used to claim a foreign tax credit in the NR’s domestic tax return. A NR’s income tax return may be filed at any time – it is not necessary to wait until the end of the Australian fiscal year (30 June).

For further information or assistance in relation to the above, please do not hesitate to contact Michael Roseby of Roseby, Rosner and Young, Melbourne.

Tel +61 3 9823 3366 Email msr@rosroy.com.au